On November 28 I welcomed the first million enrolees under ACA, whether to marketplace policies or Medicaid/SCHIP. The post was based on the fragmentary data available at the time, brought together in Charles “brainwrap” Gaba’s invaluable running spreadsheet, with some extra tweaks and guesswork by me.

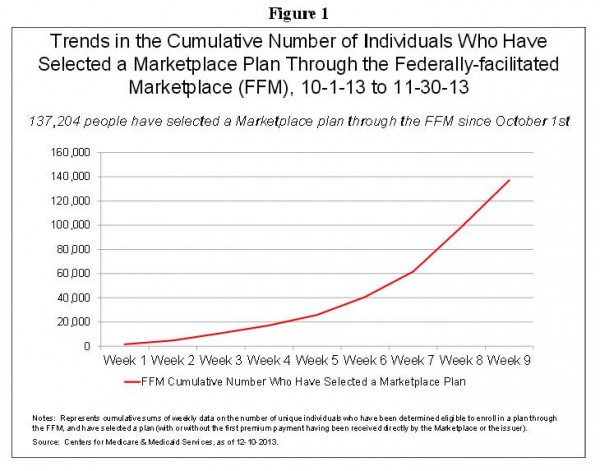

HHS has just released its ACA enrolment report to 30 November. It even has a chart! Heavens to Betsy! Here’s the rare bird (click for better resolution):

How did I do?

- My headline number: one million.

- HHS:Â “Number of Persons who have Selected a Marketplace Plan or had a Medicaid/CHIP Determination or Assessment: 1.2 million”.

My point. But on the more detailed predictions, I didn’t do nearly so well.

- Me: “New enrolments in private insurance and Medicaid/SCHIP will together be well over 2 million, and more probably over 2.5 million.”

- HHS: 1,168,000. (All numbers rounded to nearest 1,000)

and:

- Me: “Over 1 million will be through private policies.”

- HHS: 365,000 (healthgov 137,000, state marketplaces 227,000)

Oops. Where did I go so wrong?

I made four adjustments to brainwrap’s data. The first three - taking out those transferred administratively from state low-income health plans to Medicaid, which HHS doesn’t count either; extrapolating the interim data from the state websites to the end of the month; and extrapolating healthgov Medicaid enrolments in the same way - were OK. They gave me an adjusted total of 1,167,000, as close to the outturn as only a fluke can be.

My mistake was grossly overestimating the number of signups to private policies on healthgov. My reasoning was that 673,000 people had eligibility determinations from healthgov on 2 November and had not yet chosen a policy. Surely they would chose one in November? Well, most of them haven’t. The total signups in November were only 110,000.

The number of such ditherers on healthgov has risen to an impressive 1,388,000, plus another 554,000 on state exchanges. On the latter, ditherers outnumber signups 2:1, with considerable variation between states; on healthgov, by 10:1.

On the well-functioning websites of California, Kentucky, New York and Washington, the dithering presumably reflects free choice. On healthgov, it’s very likely that the continuing problems with the shopping stage of the website, and with its communication with insurers, pushed up the number. If healthgov had the same ratio as the state sites, I’d have been 350,000 up, and less embarrassingly wrong.

By report, healthgov really took off in December, after the announcement that it was fixed. The leaked number for signups in the first three working days was 56,000Â - half the total for all of November. It’s reasonable to think Healthgov will converge on the mean delay on the state sites, and that the latter will fall as deadlines near.

What of my third prediction?

- Rick Perry, Rick Scott, and all the other GOP politicians betting on Obamacare to fail will have egg on their faces.

No egg is visible in their mirrors of course. Those conservative critics with an open line to reality are reduced to whingeing: people aren’t really enrolled until they pay the first premium (that must come as a shock to many!), there’s a big hill to climb to meet the March goal, etc. (Cf. Sybil Fawlty, “special subject - the bleeding obvious”. )

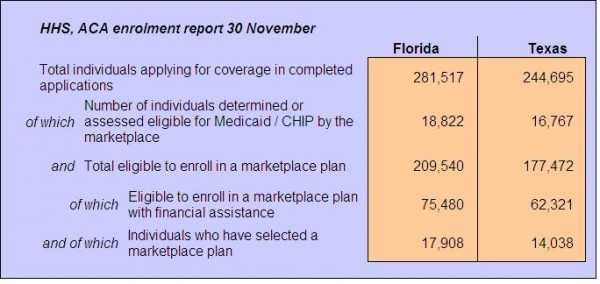

No news from Perry or Scott. Perhaps they are glumly contemplating these numbers in the HHS report:

It’s only going to get worse for them. Jeffrey Zients has saved the Affordable Care Act and with it Barack Obama’s legacy. I Told You So.

Update - postscript:

Zients may be a managerial genius, but he doesn’t know anything about visual presentation. Look at the difference I was able to make to the Florida and Texas data just doing three things: getting rid of the grocer’s Initial Caps; changing the order, so that Medicaid goes before the rows on marketplace policies; and indenting to give a sense of the nesting of the data. Basic stuff. The most important policy achievement of the Administration deserves far better. Zients should hire someone who has read and digested Tufte.

Update 2: 15 December

As a crosscheck on the very marked December acceleration in signups on healthgov, California have released recent data showing the same effect:

In the week of Dec. 1-7, an additional 144,146 applications for individuals (averaging 20,590 per day) were completed, and 49,708 individuals selected plans (averaging 7,100 per day).

Since the California website has worked well from the outset, their enrolment speedup presumably reflects decision-making by applicants, not the removal of technical logjams. Ockham’s Razor suggests that the same dominates at healthgov.

Brainwrap’s running unharmonised total of private policy signups today is 685,915, a remarkable 86% increase on the harmonised HHS total on November 30. I’m going to stop following this, game over.

People who post when they are wrong (and right), and why. Impressive.

Keith,

You’ve omitted the more important number, and I believe it is the number that will leave visible egg on Governors Goodhair and “I’m not a crook” Scott’s faces.

That number is the number of persons who are not eligible for Medicaid under the current Texas and Florida rules, but would be eligible under the expansion. By and large, these people cannot afford the market policies even with the premium supports. These people (and others like them in other GOTP controlled States) will be the new, identifiable group of uninsured.

I hope and pray that Census and BLS have modified their questionnaire for the 2014 March Supplement to collect the information that will allow them to specifically identify these people.

Has any commenter seen an estimate? You can get an impressionistic handle by comparing Florida with New York - they have almost the same population (19,318,000 to 19,579,000). Healthgov has determined 19,000 Floridans to be eligible for Medicaid/CHIP under the old standards, or 5.7% of applicants; New York’s state site has found 53,000 under the new expanded standards, or 17.8% of applicants. So as a quick rule of thumb, the expansion makes at least an extra 10% of applicants eligible for Medicaid/CHIP.

I don’t think I agree with your analysis politically. In human terms, you are right - the denial of expanded Medicaid is an avoidable tragedy; but the excluded aren’t by and large Republican voters. But many of the citizens applying for policies and getting subsidies were Republicans at the last election. There’s no sign of a boycott. Some percentage are no doubt coerced into buying coverage they don’t want, but it must be small, especially in Florida. Larger numbers are benefiting in very concrete ways. By refusing to set up state exchanges, Scott and Perry have ensured that Obama got the temporary brickbats for the botched rollout, now receding (in Krugman’s phrase) in the rear-view mirror - and will now get the credit for the long-term gains.

James

My anecdatal impression is that income in Florida is probably skewed to the left of the bell curve versus New York.

Yup. New York is a rich state. I did write “at least 10%” for my rule of thumb.

The Kaiser Foundation did an estimate. Florida, 763,890. Texas, 1,046,430. Always look to the Kaiser Foundation for US health statistics; they’re good.

http://kff.org/health-reform/issue-brief/the-coverage-gap-uninsured-poor-adults-in-states-that-do-not-expand-medicaid/

Well. it looks like the ClimateGate Hockey Stick, so it must be a hoax.

Good joke, but of course it doesn’t really. What is surprising is that it’s a near perfect exponential curve - which is what you would expect to see if the federal website had worked perfectly from the beginning. Are we all responding to something that was always entirely about perceptions, and the pain of a minority? Can you get a curve like this simply from the progressive removal of randomly distributed bugs in the software?

Yeah, let’s have a reality check:

1. It’s a curve of people who’ve left a plan in their “cart”, which is the only way to get a final price. It’s not a curve of people who’ve actually gotten insurance, and undoubtedly includes a lot of people who got that final price, and left in disgust without clearing their cart, or whose efforts to obtain insurance failed for other reasons.

2. HHS says the number includes an unknown proportion of duplicates. The real number is smaller, by an unknown percentage. And #1 applies to that smaller, real number.

Indeed, the administration is already proceeding with setting aside still more black letter implementation dates, and is now urging insurers to waive filing deadlines, and extend insurance to people who haven’t paid yet, in an effort to paper this over.

The original rollout was more of a screwup than even the ACA’s opponents expected, some degree of improvement was unavoidable, just because it started out so bad. But, at the current rate, we might be where we were supposed to be now, some time late next year. Which is like saying that you expect the flight computer on the airliner to finish rebooting in ten minutes, when you’re thirty seconds from the ground.

Wouldn’t be such a problem if the President hadn’t been lying about people getting to keep their insurance if they liked it, but isn’t so great given how many people are going to lose their insurance on January 1st. Millions.

Well, the whole thing was a terrible idea from the start, but at least it’s coming to a head just before the 2014 elections, despite the desperate efforts to push the consequences past another election cycle. Might actually have to pay the piper this time.

Brett: your point 1 is pretty clearly false. A signup is not “left in the cart†but the equivalent of a confirmed order on Amazon before the credit card payment clears. It’s a statement of contractual intent made to an insurance company. As always in insurance, the contract enters into force with the payment of the first premium. As a talking point, it’s merely silly.

Point 2 is CYA footnote stuff by the HHS statisticians, in case they have to issue corrections later. The Oregon website, say, has been totally screwed by Oracle, and the state is resorting to ad hoc paper methods. You offer no actual evidence – say press reports of applicants getting two bills from the same insurer – that duplicate signups in the state exchanges are a significant problem as opposed to a hypothetical small error signal in the data.

Your “lying†talking point is totally off topic and has been exhausted elsewhere. I can’t sensibly delete part of a comment, and the rest is on topic. I ask other commenters not to feed this trollery.

In about 16 days, the issue will be difficult to argue about, the number of people with coverage will either go up, or go down. Coverage will either improve, or decline.

I have no doubt most Democrats will find some way to blame all the consequences of the ACA and the administration’s policies, (Not identical, in many cases the latter violates the former.) on insurance companies. This, after all, is the point of treating insurance companies like sock puppets, instead of directly doing things through the government: So somebody else takes the blame.

Brett: I’m glad to see you are now on board with single payer. But I don’t see what’s so wrong with sock-puppeting insurance companies, that is treating them as regulated utilities.

I have yet to be fined for not buying the product of a regulated utility. There would be no tax penalty if I stopped using electricity, or produced my own. No fine if I disconnected from the water system. Not a quarter mile from here, people are relying on wells and septic fields, and not breaking the law by doing so. Even where a product is sold by a regulated utility, other companies are free to sell it, too.

Contrast this to what the government is doing to the insurance companies: Forcing people to buy their product, while forcing the companies to sell it on the government’s economically irrational terms. Dictating what they must sell, and may not.

No, I’m not on board with single payer, but I recognize what Democrats have done: They have instituted something vaguely like single payer, only using the insurance companies as intermediaries, with the intent that they take the blame for everything that goes wrong.