In this first installment of one of Harold Pollack’s “Curbside Consult” interview series for healthinsurance.org, Harold and I discuss the changing mental health needs of veterans, the myth that drug illegality is the cause of opioid overdoses, the role of alcohol in violence and incarceration, and the effectiveness of Alcoholics Anonymous.

Portrait of a dead lady

Ghirlandaio’s 1488 portrait of a young Florentine noblewoman has become the signature piece of the Thyssen-Bornemisza museum in Madrid:

Her name was Giovanna degli Albizzi Tornabuoni. Both parts of her surname mattered at the time. The Albizzi were rivals of the Medici, the Tornabuoni the Medicis’ right-hand men. Her marriage two years earlier to Giovanni Tornabuoni was a political one, a burying of the hatchet between powerful clans. The Tornabuonis were clearly proud of the catch and celebrated her beauty and status in this lovely portrait.

The melancholy Grecian-Urn atmosphere created by the rigid pose and sombre background with pious knick-knacks is no accident. Giovanna died in childbirth, aged only eighteen, the year of the portrait. (Was it begun in life? I’ve suggested to the museum an X-ray to see if Ghirlandaio began with a more cheerful background of Tuscan hills or a rich interior. I’ll let you know if they take me up.)

The beautiful Giovanna can therefore represent all the young women who have paid the ultimate price for our dangerously large brain cases. Continue Reading…

Why both Liberals and Conservatives need a health reform deal

On December 16, 2010 I wrote a post that began:

While the rhetoric around health reform has been incendiary from day one, in policy terms, a compromise between Democrats and Republicans using the outline of the Affordable Care Act (ACA) has always been available. The two primary problems with the health care system are costs and lack of coverage. The ACA does pretty well on the second, and is a start on the first, but much more is needed. It will be very hard to get a handle on health care costs, and we will likely only succeed in doing this if both parties are on board.

I then proposed the outlines of a deal:

- Federally guaranteed catastrophic coverage implemented via Medicare

- Private insurance sold in state-based exchanges for gap amounts if individuals desired more coverage, with income based subsidies

- Federalizing the dual eligible Medicaid costs, and moving over time to buy low income persons into subsidized private gap insurance, thus transitioning the low income portion of Medicaid over time

- ending the tax preference of employer paid health insurance; make all subsidies explicit Continue Reading…

FTD (not the florist)

About 18 months ago I shared the news that my family was moving to another house so that my mother in law could move in with us.

This move took place about 16 months ago, my mother-in-law’s house sold about a year ago and she moved into our new house last Summer. Her physical and cognitive decline since that time has been pronounced, and she was hospitalized 3 times in 40 days from Thanksgiving to Christmas; the last hospitalization occurring when she wandered from our house during the night for the third time that last 10 days she was with us. She fell in a ditch by a road near where we live, was found by a runner just before dawn, and was “Jane Doe” for around 4 hours in the ER before we realized that she was gone.

The Dramatic Arrival of Health-Oriented Drug Policy

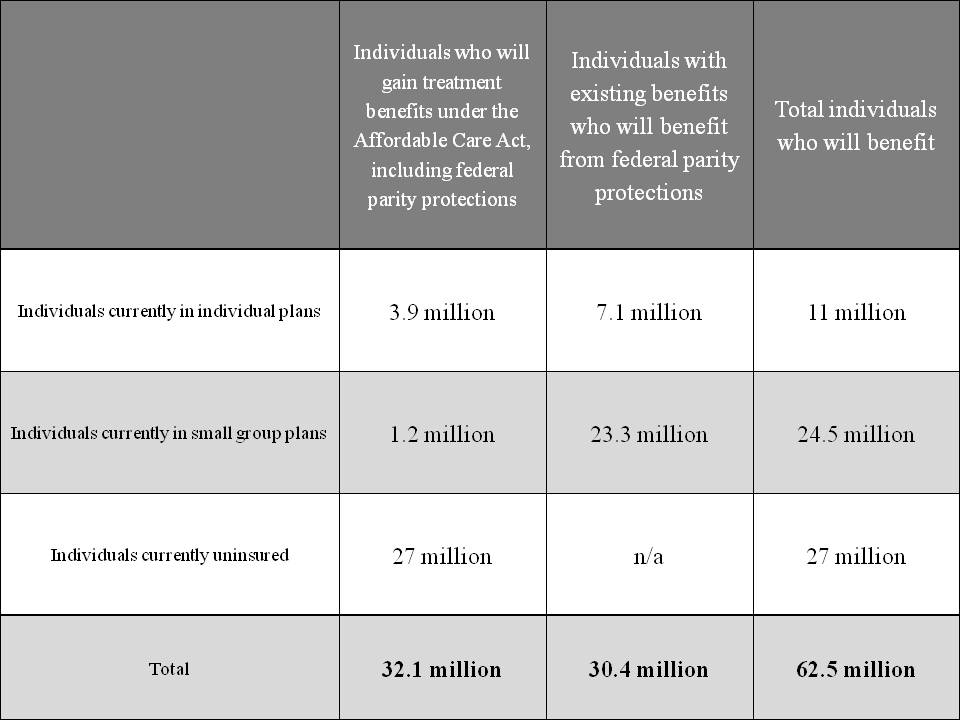

Given how often some people demand “health-oriented drug policy” from the Obama Administration it is more than a little peculiar how one of the biggest reforms in history didn’t attract more attention and draw more praise in the blogosphere. With the Administration’s declaration that treatment of mental health and substance use disorders are essential health care benefits, to be provided not only in the state health insurance exchanges but in all new individual and small-market health insurance plans, over 60 million Americans just got better insurance coverage for these disorders. The graphic below is from HHS:

That isn’t the end of the good news. The more than 100 million Americans who receive coverage under large-group plans are also getting better coverage due to the Mental Health Parity and Addiction Equity Act. Passed in the waning days of the G.W. Bush Administration with the regulations being written by the Obama Administration, the law mandates that any offered benefits for addiction and mental health must be comparable to those offered for other conditions.

But wait there’s more: Medicare, which enrolls almost 50 million people, has long had inferior coverage for addiction and mental health outpatient care, reimbursing only 50% of costs versus 80% of those for other forms of medical care. Thanks to a provision in the 2008 Medicare Improvements for Patients and Providers Act (again, give it up for the 110th Congress and President Bush), this disparity in reimbursement is being phased out and will be entirely eliminated by January 1 of next year.

When you consider that addictions almost always evidence themselves in adolescence or early adulthood, it becomes clear that the ACA provision allowing parents to keep children on their insurance until age 26 adds yet another layer of protection for the population.

Some people of course have coverage from more than one of the above sources, but even granting that overlap, over 200 million Americans have gotten improved insurance coverage for treatment of drug and alcohol problems (and mental health disorders as well). This includes many people who were starting with nothing, as well as a large population that had a benefit of inferior quality.

This is the biggest expansion to access to care for addiction in at least 40 years and probably in American history. In financial terms, it is certainly the biggest commitment of public and private resources to the health care of people with substance use disorders in U.S. History. Congratulations are in order to countless grassroots advocates, civil servants, political appointees, members of Congress and two U.S. President for transforming the face of health care for addiction.

Medicare’s ‘improve or you’re out’ rehab policy

I have been meaning to write about the important court order overturning Medicare’s longstanding ‘improve or you’re out’ (of Medicare financed SNF and/or home health) policy for rehabilitation services. Basically, beneficiaries who had plateaued and could at best maintain function could not receive rehab services under these parts of the Medicare benefit package. Medicare has settled the court ruling with plaintiffs to expand the availability of these services, even to patients who cannot show improvement, but only maintenance of function. Several quick points:

- While this issue has long been on the radar of elder/disability advocates, it never made it into the popular culture as a political issue. Why? I think it is related to the fact that long term care and disability are the underside of the health care system and people don’t like to think about needing rehab just to be able to maintain their ability to swallow, for example. Not an attractive thought.

- Imagine if Medicare announced that chemotherapy X to treat Cancer Y would only be paid for if you could prove it was extending your life. The internet and the health policy meets political corner of twitter would break. We turn in horror from looking at long term care, but run toward the potential denial of a curative therapy and have a group freak out (sorta like ‘rubber-necking’ at a bad car wreck).

- It doesn’t bother me and I even like the fact that the question of ‘can/is this person benefiting?’ from rehab services is being asked. It is a policy question as to whether such care should be required to bring about improvement, or simply to maintain function. I think the case has now been rightly decided toward expansiveness of these services. However, the same type of bright lights (does it extend life, improve function, how much does it cost?) should be asked of the entirety of the Medicare program. Not just the parts no one likes to think about.

cross posted at freeforall

Community Reinvestment Comes to Health Care

I have no idea what the nonprofit community would do without Rick Cohen of the Nonprofit Quarterly: if there’s an issue affecting nonprofits he’ll have a fresh and useful perspective on it, and this article about the Community Health Needs Assessments required by the Affordable Care Act is no exception.

What struck me most was Cohen’s point that CHNAs could do for health care what the Community Reinvestment Act did for real estate lending: make large institutions pay attention to the communities where they do business. Whatever its weaknesses, CRA did make a serious dent in the once-common practice of red-lining, refusal to lend in poor neighborhoods, and we can expect CHNAs to make a similar change in the culture of nonprofit hospitals. Simply providing an emergency room isn’t sufficient community service, and if a nonprofit hospital fails to grasp that it jeopardizes not only its Federal health-care dollars but the tax-favored status of the rest of its income. We know that because the provision calls for enforcement by the IRS as well as the Department of Health and Human Services.

This sort of positive pressure from the legislature to improve community health services is far more effective than the purely negative pressure courts can supply by rejecting a hospital’s claim of charitable status (as in the Provena case in Illinois). Because the point isn’t to play “gotcha” with nonprofit hospitals—it’s to supply communities with the maximum benefit possible from the health care resources already available.

Once again the more you know about the Affordable Care Act, the better you like it. And “Obamacare,” intended as an epithet, sounds more and more like a well-deserved tribute.

cross-posted with The Nonprofiteer: www.nonprofiteer.net

The cost of contraception

I think Kevin Drum - about the smartest blogger, or journalist of any description, now working - makes a mistake from time to time just to keep the rest of us on our toes. He’s right that the latest Administration plan to deal with contraceptive coverage under employer-paid health insurance is a kludge, and he’s right that, since money is fungible, sayingthat insurance companies have to spend some money other than the employers’ money to cover it is gibberish. (That’s supposed to insulate the employers from the moral onus of allowing reproductive freedom rather than imposing their dogma on their employees. I forget who it was who Tweeted the question, “Should health insurance provided by a Jehovah’s Witness employer cover blood transfusion?”)

But what Kevin misses is that offering health insurance with contraceptive coverage is not in fact more expensive than offering health insurance without it, because if the woman gets pregnant the insurer will have to pay for prenatal care and delivery. You can cover a lot of $50 contraceptive-pill prescriptions with the avoided $10,000 cost of a single uncomplicated delivery.

As to the plan itself: looks to me like a perfect non-solution to a non-problem.

Update Kevin points out a complexity I’d missed. Yes, total health care costs go down with contraception. But if enough women without coverage pay out-of-pocket for the Pill, the insurance company could still come out ahead by stiffing them (while covering Viagra, of course). That leaves a factual question: if a big employer goes to a health insurer and asks for a quote for employee coverage, is the quote actually lower if contraception is excluded?

Second update Kevin produces a reasonable-sounding BOTEC suggesting some net cost to insurers. Which means he still owes the rest of us one mistake.

Genetic Nondiscrimination Act of 2008 and LTC Insurance

NPR has a story on the legal use of genetic information to discriminate (underwrite, set premiums) in the private Long Term Care (LTC) insurance market. I am the first author of the paper that Bob Green (the P.I. of the underlying study) is discussing in the NPR piece and I have blogged about its findings here and here.

The basic story of the paper in Health Affairs is that persons with at least one copy of the e4 variant of the APOE-4 genotype were found to be both more likely to move to a nursing home in a community cohort of elderly persons living in 5 N.C. counties, as well as being found in the REVEAL II study to alter their behavior upon finding out they were at increased risk of AD, including making changes such as buying Long Term Care Insurance. In short, this is adverse selection whereby consumers have information that companies do not, a story that likely keeps insurance executives up at night.

Put Obamacare On The Table!

Kevin Drum notes that Republicans insist on something called “entitlement reform,” but have no actual ideas about what this reform might mean (aside from getting rid of Medicare). So now they are insisting that President Obama make the first offer, which is a laughable position. The also insist on “putting Obamacare on the table”, which the White House immediately rejected.

But maybe it shouldn’t. If we’re talking about reducing entitlement payments, wouldn’t it be great if we could find something that could save, say, $500 billion over ten years, but not reduce access to coverage and actually make the health care system more efficient?

Oh wait: we do! Remember the public option? That’s what it would do, according to the Lewin Group and the Urban Institute. Both studies estimated a public option at saving the federal budget $50 billion a year. And if anything, those estimates are conservative, because they do not assume that Medicare providers would be mandated to accept public option patients (as they should be), and they also assume large “cost shifts,” i.e. increases in private insurance costs, which have no empirical basis. So I say put Obamacare on the table and put in a strong public option.

What’s that you say? That such an action would reform entitlements and save money, but that the Republicans would never go for it? Gosh, it’s almost as if the GOP doesn’t really care about saving money and really only wants to cut people off of health insurance. I can’t imagine why anyone would think that.