Brad Flansbaum sent me a link to a private score of PCARE, the reform plan released on Monday by Republican Sens. Burr, Coburn, and Hatch. I don’t know the Center for Health and the Economy, though I do know several members of their advisory board and many of you will as well. I don’t have my own simulation model to be able to verify these sorts of results, and the CBO is the final word, but I will just assume that a group that has Uwe and Holtz-Eakin on the Board must be somewhat credible. There is much to be learned here, even if you assume this to be an overly optimistic score.

First off, lets just say that the rage machine that has been perfected to argue against the ACA could get plenty cranked up from the these results. There is a breathless Americans for Prosperity Ad running in North Carolina talking about a nice lady losing her doctor in an Obamacare plan, in health policy speak, due to the rise of the narrow network. Yep, this score says PCARE will have a slight increase in persons covered by 2023 compared to the ACA, but most of that arises from a shift of people into narrow network plans.

Now narrow network plans don’t bother me one bit (I thought everyone wanted to reduce costs!), but the ad machine that is trying to give the Republicans the Senate in 2014 is demagouging something that is a feature and not a bug of the plan put forth by Republican Sens. Burr, Coburn, Hatch. They achieve coverage expansions via an increase in individual based coverage (up 30% by 2023) at the expense of employer sponsored coverage (down 2% by 2023) and Medicaid (down 11% by 2023). What impact does this shift have on access? They calculate a “Provider Access Index” that identifies the degree to which persons insured by different options can pick the providers they want and they say:

With respect to patient’s access to their providers of choice, the CARE Act is expected to achieve similar access to current law, based on the H&E Provider Access Index (PAI).[6] The proposal is projected to reduce the average PAI in the individual market, due to an influx of consumers enrolling in low-cost narrow network plans. However, that reduction is offset by a reduced reliance on Medicaid to insure the low-income population.

On premiums, the analysis says they will be generally lower in the non employer market, but most of the decline is among individuals and not families.

By 2023, the proposal is expected to yield substantially lower premiums than current law in individual insurance product categories with savings of 2 – 11 percent for single policies. H&E predicts that family policies will see a modest decrease ranging from 0.3 – 1 percent.

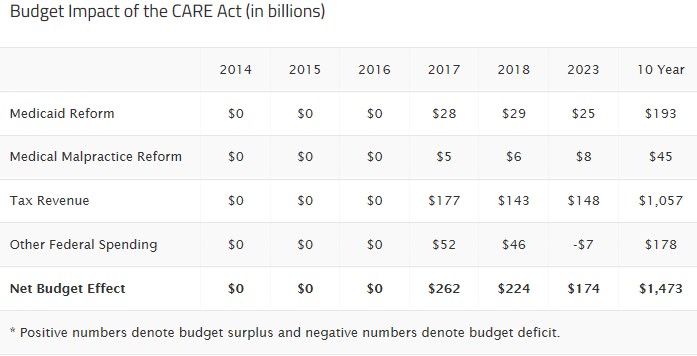

On the overall federal budget, they expect a 10 year reduction as compared to current law (ACA), a reduction of about $1.5 Trillion over 10 years. This is actually consistent with the co-sponors saying the plan will be “roughly revenue neutral” because of how large the federal budget is from 2014-2023 ($46.7 Trillion, see p. 8), the appropriate denominator to have in mind. For example, CBO’s budget forecast over the same period was reduced by ~$618 Billion just from their February, 2013 to June, 2013 estimates! It is illustrative to look at the components of the estimated deficit reduction from passage of PCARE over the 10 year window:

Yep, most of the action is achieved by the capping of the tax exclusion of employer sponsored health insurance. You know what this would be called if this (good in my opinion) policy were to replace the cadillac tax in the ACA? A Trillion dollar tax increase (Ah-Trill-Yun! with scary music in the background). The Medicaid changes which will result in blood on the floor debate yield around $150 Billion in savings over 10 years, and the savings from medical malpractice reform are essentially a rounding error in the context of the 10 year federal budget.

So, this score says that PCARE will achieve similar levels of insurance coverage as the ACA by 2023, and will result in a reduction of the federal budget as compared to the ACA, primarily by shifting people into narrow network private insurance plans, and increasing taxes of persons with generous employer sponsored health insurance. It doesn’t analyze the generosity of benefits covered (at least that I can tell, but they had to make assumptions), nor does it identify the impact on out of pocket costs that will result in these coverage levels; these are important items to understand, especially given that there are no proposals about transitioning to different models of care and the like.

Taking a look back in time through the lens of this proposal, I can’t help but thinking that Sens. Burr and Coburn missed a big opportunity in January 2010, by not throwing Sen. Olympia Snowe a lifeline (remember, she voted for ACA out of the Senate Finance Committee), which would likely have brought along Sen. Collins. Those four together could have gotten a lot once Scott Brown was elected. Instead they choose full opposition, and gross over-statements in their arguments against the ACA, especially given the proposal they now put forth. In the end, they helped to create and exacerbate the political culture that will make it so hard for their proposal to be given the subtle, and nuanced listen that it deserves.

***

Update: I am trying to get details of the model, assumptions and the like. I have requested it officially for the site that put out the score. I have also been talking on twitter with members of the Advisory Board. I think the model is an update of Steve Parente’s model (old one, paper likely behind new one). Will confirm/clarify as I get info.

Update 2: I confirmed that Steve Parente did the simulation. Here is a pdf of the paper linked above Parente.hesr_12036 behind the model, published in HSR. However, it is based on ACA uptake after SCOTUS ruling, so I am still trying to understand PCARE assumptions; Steve and I are going to talk.

Update 3: Loren Adler has 7 important questions/points in his twitter timeline about detail gaps in the private score. I have conversed quickly with Steve Parente via email, but don’t have enough yet to clarify. I will likely do so in another post when I understand more.

cross posted at freeforall

Don you and Austin are being so open minded on this plan that your brains are falling out. As Edwin Park notes at CBPPits not even clear that there is community rating anywhere in this plan, or if such a thing would even be possible when there are no minimum benefits. The poor and those with pre-existing conditions seem like they would get stuck with much higher premiums.

One problem for moderate Republicans (it’s a surprise to discover that they still exist, at least for white paper purposes if not actual votes) is that they are all committed to the party line of “repeal and replace”. This means that any GOP health bill whatever has to be another 1000-page brick. Lining up the votes behind any such comprehensive package looks impracticable.

The long gestation and difficult birth of ACA are now its defences. Republican health proposals will only deserve to be taken seriously when they drop the repeal demand and limit themselves to bills for reform of what is now, like it or not, the framework for American health care.

The purely partisan side of me really wants the dems to rip this thing apart as a huge tax increase but I know they will never do anything that self-serving. Instead they should call a big hearing and have these senator sit there in front of the cameras while they rip them apart. Would be fun theatre.

Signed

Pottifar, DS, MBH, MP, ASCP, MS, BS, PhD, DPSY, MPH, MBA

Insurance claims achievement can be a heck of task as this may go through long years of trial and settlement issues. Lawsuits filed with professional law firms can benefit the personnel affected with medical malpractice and get liability benefits in the form of huge amounts even though this will just act as a relief. Check out this case study http://www.sommersandroth.com/our-cases/parents-o… where parents of a disabled boy recovered $11.8 million due to delay in recognizing placental abruption.

nice post